Probability Distributions > Hyperbolic Secant Distribution

What is the hyperbolic secant distribution?

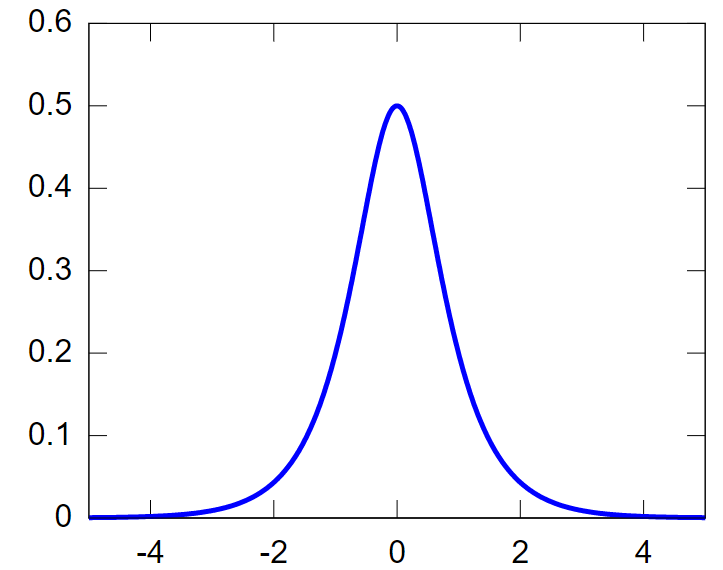

The Hyperbolic secant distribution (also known as the inverse-cosh distribution or sech distribution) is a bell-shaped, symmetric probability distribution with a mean of 0 and variance of 1. It is a continuous distribution that is tractable (computationally efficient to work with), which means computer calculation of the distribution at any point can be performed in a reasonable amount of time.

This distribution is derived from the hyperbolic function. It looks a lot like the normal distribution; both distributions have a density proportional to their characteristic functions, but the hyperbolic secant is leptokurtic with heavier tails.

The hyperbolic secant distribution is a member of both the location-scale and exponential families.

- Location-scale family members can be parameterized by a location parameter (μ) and a scale parameter (σ). This means that the distribution can be shifted and scaled to fit different data.

- Exponential family members share certain mathematical properties. For example, their probability density functions (pdfs) can be expressed in a specific canonical form.

This dual membership makes the hyperbolic secant distribution a versatile and useful tool in statistical modeling.

Hyperbolic secant distribution pdf

A random variable X = ln|Y1/Y2| follows a hyperbolic secant distribution (where Y are normal random variables). The density of the distribution is proportional to the hyperbolic secant function, the reciprocal of the hyperbolic cosine function defined by [2]:

cosh(x) = 0.5 [ex + e-x]

The pdf of the hyperbolic secant is [3]:

Where μ ∈ ℝ and σ > 0 and

The sample mean and sample median are equally efficient estimators for the population distribution.

The Hyperbolic Secant distribution is not as well known as other exponential family distributions due to its isolation from many well known statistical models [4]. It does bear some similarities to the normal distribution both in shape and symmetry. Both distributions have a density proportional to their characteristic functions although the hyperbolic secant has slightly heavier tails [5].

Use of the hyperbolic secant distribution

As noted above, the hyperbolic secant distribution’s pdf can be computed rapidly, which is useful for simulations and optimization problems. It’s symmetry eases interpretation of results. The likelihood of extreme values makes it useful in modeling phenomena with a wide range of values, such as stock prices or weather patterns.

The Hyperbolic Secant distribution is widely used in many fields, including.

- Finance, where it can model volatility in financial markets. Its robustness to heavy tails and skewness makes it ideal for capturing extreme market outcomes.

- Engineering, where the distribution has been used to model failure times of mechanical systems.

- Physics, where it can be used to describe the distribution of energies or momenta in particle physics.

The Hyperbolic Secant distribution may not be seen as often as some other distributions due to its isolation from well-known statistical models [2], but it can be a useful tool for modeling phenomena with wide ranges of values and heavy tails. Its easy computation, symmetric and platykurtic properties, and application in various fields make it worth considering for statistical analysis.

References

- Image: IkamusumeFan, <https://creativecommons.org/licenses/by-sa/4.0>CC BY-SA 4.0 , via Wikimedia Commons

- Stat 5601 (Geyer) Hyperbolic Secant Distribution. Retrieved December 18, 2021 from: https://www.stat.umn.edu/geyer/old02/5601/examp/hsec.html

- Rubio, F. The Hyperbolic Secant Distribution. Retrieved December 18, 2021 from: https://rpubs.com/FJRubio/HSD

- Ding, P. (2014). Three Occurrences of the Hyperbolic-Secant Distribution. Retrieved December 18, 2021 from: https://arxiv.org/abs/1401.1267

- M. J. Fischer, Generalized Hyperbolic Secant Distributions, 1

SpringerBriefs in Statistics, DOI: 10.1007/978-3-642-45138-6_1