< List of probability distributions < Benini distribution

The Benini distribution (also called the log-Rayleigh distribution), is a continuous probability distribution often used to model failure rates in actuarial science and income distributions in economics.

The distribution is named after Italian statistician and demographer Rodolfo Benini [1], who proposed the distribution as an alternative to the Pareto distribution. The Pareto assumes a linear relationship while Benini’s distribution assumes a quadratic fit — a second order polynomial — which Benini found was a better fit for income-size distributions [2]. Sphilberg independently obtained the same distribution when modeling fire accident loss amounts [3].

Benini distribution properties

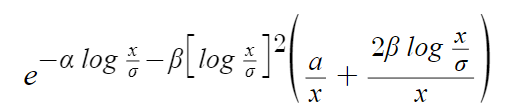

The probability density function (PDF) is defined as

Where

- α and β are shape parameters and

- x0 is a scale parameter.

Setting β = 0 in the Benini PDF results in the Pareto distribution.

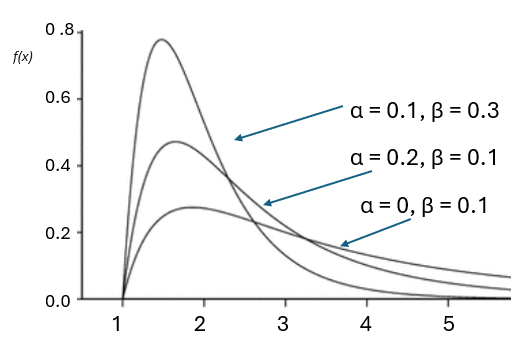

Two shape parameters, α and β, control the behavior of the PDF. These two parameters can result in a wide variety of different PDF shapes including fat tails or thin tails. The PDF might be monotonic decreasing, or unimodal with singularities approaching the left domain boundary [4].

The location parameter (x0) controls the location of the PDF on the x-axis; it also acts as a scaling parameter because low values of σ correspond to more peaked graphs compared to high values of x0, which result in flatter graphs. Note: Some authors use σ for the location parameter (e.g., [4, 5]).

The cumulative distribution function (CDF) is

1 – e–α log (x/σ) – β[log x/σ]2 .

Benini distribution vs. lognormal

The Benini distribution is similar in density to the lognormal distribution — a widely known example of a distribution that is not determined by its moments, although all its moments are finite [6]. This similarity of the two distribution’s densities suggests that the Benini distribution might also have this pathological property [5].

The moment problem is a challenging issue in probability theory that questions whether the expected values of a probability distribution solely establish its distribution. The expected values, or moments, are derived from powers of the random variable. Research has shown that the moments of the lognormal and the Benini distribution do not adequately determine their respective distributions. This implies that there are multiple distributions that share the same moments. This can pose challenges in certain applications. For instance, estimating the parameters of a Benini distribution from data cannot be accomplished solely based on moments of the data.

References

[1] Benini, R. (1905). I diagrammi a scala logaritmica (a proposito della graduazione per valore dellesuccessioni ereditarie in italia, francia e inghilterra). Giornale degli economisti, 30:222 231.

[2] Vaidyanathan, V. Benini Distribution: A Less Known Income-Size Distribution. Special Proceedings: ISBN#: 978-81-950383-0-5 23rd Annual Conference, 24-28 February 2021; pp 93-99

[3] Shpilberg, D. (1977). The probability distribution of fire loss amount. The Journal of Risk and Insurance, 44(1), 103-115.

[4] Wolfram Research (2010), BeniniDistribution, Wolfram Language function, https://reference.wolfram.com/language/ref/BeniniDistribution.html (updated 2016).

[5] Kleiber, Christian (2013) : On moment indeterminacy of the Benini income distribution, WWZ Discussion Paper, No. 2013/08, University of Basel, Center of Business and Economics (WWZ), Basel, https://doi.org/10.5451/unibas-ep28620

[6] Heyde, C. C. (1963): “On a Property of the Lognormal Distribution,” Journal of the Royal Statistical Society, Series B, 25, 392–393.