The Waring distribution is a generalization of the Simon-Yule distribution, allowing for more flexibility and greater accuracy when modeling data. To put that another way, the Simon-Yule is a special case of the Waring distribution when the parameters take on certain limiting values. It is sometimes linked to the Pareto distribution, because the tails show Pareto-like behavior.

The Waring has two parameters (α and β); The generalized form has an additional parameter ν.

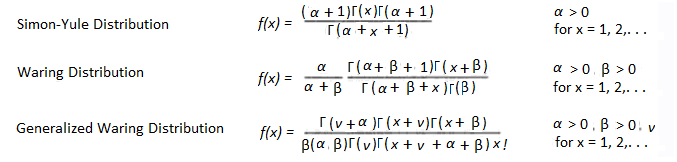

Waring distribution, Yule-Simon, and generalized Waring pdfs [1].

The Waring Distribution is a theoretical distribution with several applications in statistics, finance, engineering, computer science and economics. It is especially useful in regression analysis due to its ability to accurately model nonlinear relationships between variables. It can also be used in hypothesis testing since it allows for higher levels of accuracy than traditional parametric tests such as t-tests or F-tests.

The Waring distribution can be an invaluable tool for predicting future trends or patterns in data sets with high variability or nonlinearity. For instance, if you have a dataset with high variability that contains sales figures from different stores over time, you could use the Waring distribution to forecast future sales figures more accurately than would be possible with traditional parametric methods.

Other than a few use cases, the Waring isn’t suitable for modeling a wide swath real-life data. Sichel, as cited in [1], states that it has

“…linear tails in a logarithmic grid, and hence [is] unsuitable for representing the upper tails of most observed biometric size-frequency data.”

Disambiguation

The term “Waring Distribution” usually refers to a generalization of the Yule distribution, but many variants on the name exist, so it can get a little confusing. To add to the confusion, subtle changes in the generating mechanism for the Simon-Yule distribution (a.k.a. a specific form of the Waring) lead to various other distributions (e.g. the Poisson distribution). The generalized Waring distribution is sometimes called the beta negative binomial distribution.

When working with this distribution, make sure you understand the context. For example, in the Wolfram documentation, “Waring-Yule Distribution” refers to the Yule–Simon distribution:

WaringYuleDistribution[α] represents the Yule distribution with shape parameter α.

WaringYuleDistribution[α,β] represents the Waring with shape parameters α and β.