< List of probability distributions < Delaporte distribution

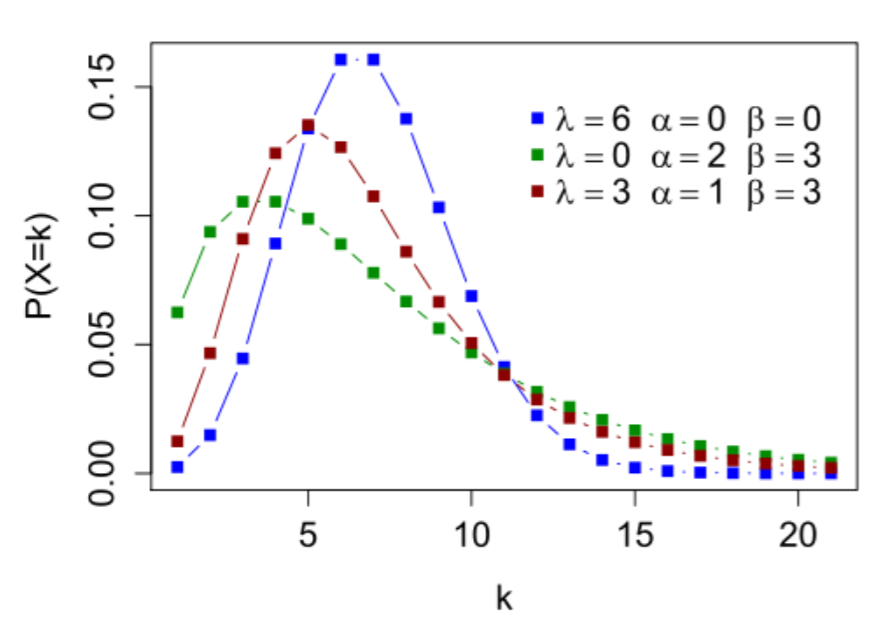

The Delaporte distribution, also called the Poisson*negative binomial distribution, has gained popularity in actuarial science as a way to model certain events, such as the expected number of insurance claims during a time period. This discrete probability distribution can be defined as a special case of a mixed Poisson distribution or as a convolution of negative binomial and Poisson distributions; it has less variability than the negative binomial but more variability than the Poisson. Alternatively, it can be thought of as a counting distribution with negative binomial and Poisson components.

The three-parameter Delaporte distribution has been put forward as an alternative to the two-parameter gamma mixture (aka the negative binomial distribution) [1].

Delaporte distribution properties

The Delaporte distribution has a fixed and variable component to its mean parameter, similar to how the negative binomial can be seen as a Poisson distribution with a gamma distributed random variable for a mean. Think of the Delaporte distribution as a compound Poisson distribution, where the mean parameter has two components:

- A fixed Poisson component (λ), which must be strictly positive,

- A gamma distributed component (with parameters α, β). Both parameters must be strictly positive [3].

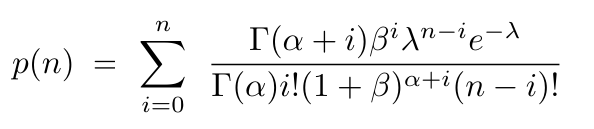

The probability mass function (PMF) is [3]:

The cumulative distribution function (CDF) is:

Other properties [3]:

- α, β λ

- Mean = λ + αβ

- Mode = z, z + 1, if z is an integer, where z = (α – 1)/β + λ; [z] elsewhere.

- Variance: λ + α β (β + 1).

Special cases of the Delaporte distribution

Special cases of the Delaporte distribution [4]:

- Delaporte (λ, a, 0) = Poisson distribution (λ),

- Delaporte (0, α, b) = Polya distribution (α, β),

- Delaporte(0, 1, b) = Geometric distribution (1/(1 + β)).

This distribution was first analyzed by Pierre Delaporte [5] in relation to automobile accident claim counts back in 1959. However, its roots go back even further to 1934 when it made an appearance in a paper by Rolf von Lüders [6] under the moniker “The Formel II Distribution.”

References

[1] Norman L. Johnson, Adrienne W. Kemp, Samuel Kotz. (2005) Univariate discrete distributions. Wiley.

[2] Avraham, CC BY-SA 3.0 US https://creativecommons.org/licenses/by-sa/3.0/us/deed.en, via Wikimedia Commons

[3] Adler, A. (2013). Delaporte: Statistical Functions for the Delaporte Distribution. Retrieved April 11, 2013 from: https://www.researchgate.net/publication/316636105_Delaporte_Statistical_Functions_for_the_Delaporte_Distribution

[4] Vose, D. Risk Analysis: A Quantitative Guide

[5] Delaporte, Pierre J. (1960). “Quelques problèmes de statistiques mathématiques poses par l’Assurance Automobile et le Bonus pour non sinistre” [Some problems of mathematical statistics as related to automobile insurance and no-claims bonus]. Bulletin Trimestriel de l’Institut des Actuaires Français (in French). 227: 87–102

[6] von Lüders, Rolf (1934). “Die Statistik der seltenen Ereignisse” [The statistics of rare events]. Biometrika (in German). 26 (1–2): 108–128. doi:10.1093/biomet/26.1-2.108. JSTOR 2332055.