Probability Distributions > Edgeworth series distribution

What is the Edgeworth series distribution?

The Edgeworth series distribution, introduced by Francis Ysidro Edgeworth in 1897, is a continuous probability distribution that approximates a non-normal probability distribution in terms of its cumulants and Hermite polynomials. It relates the probability density function (pdf) of a non-normal distribution to a standard normal distribution PDF. It is sometimes seen in statistical asymptotic theory, where approximations to sample statistic distributions of order greater than n-1/2 are calculated [1].

The Edgeworth series distribution has its roots in the study by Carl Friedrich Gauss in the early 19th century on the distribution of errors in a least squares regression, which he established to be approximately normal. Later, Edgeworth built on Gauss’s contribution, demonstrating that this distribution of errors can be estimated by a series composed of Hermite polynomials and cumulants.

Edgeworth distributions are derived from an Edgeworth series, a type of series that can be used to approximate a probability distribution. Edgeworth series are typically used to approximate distributions that are not normally distributed, such as the binomial distribution or the Poisson distribution.

Properties

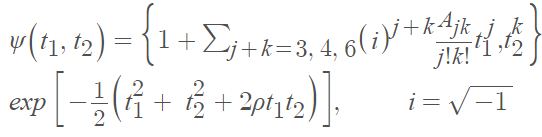

The pdf for the bivariate Edgeworth series distribution (BVESD) is [2]

Where

- φ(z1, z2) is the standard bivariate normal density function,

- Aij’s are functions of the population cumulants, and

- Dz1, Dz2 are partial derivative operators.

The characteristic function is:

It is a challenge to generate samples from the PDF of the Edgeworth series distribution. In addition, the distribution of the conditional probability of misclassification for the ESD is intractable because of the expression’s complex nature. Related to the Edgeworth form of distribution are the Cornish-Fisher expansions, although it has no general theoretical superiority [3].

Uses of the Edgeworth series distribution

The Edgeworth series distribution is a powerful tool for analyzing non-normal data. It has a wide range of applications and has been used by many statisticians and economists, including Ronald Fisher, Jerzy Neyman, and John Tukey. The distribution is versatile and widely applicable; its uses include:

- The calculation of moments for non-normal distributions;

- The construction of confidence intervals and hypothesis tests;

- Simulation of non-normal data;

- Modeling asset price distribution in financial markets;

- Calculating approximations to sample statistic distributions of orders greater than n-1/2 in statistical asymptotic theory [1];

- Studying nonlinear gust loading factors (used in the design of structures exposed to extreme winds).

References

- A. Adeyeye. Asymptotic Distribution of Probabilities of Misclassification for Edgeworth Series Distribution (ESD). Engineering Mathematics. 2020; 4(1): 1-9 http://www.sciencepublishinggroup.com/j/engmath doi: 10.11648/j.engmath.20200401.11

- S. Kocherlakota , K. Kocherlakota & N. Balakrishnan (1985) Effects of nonnormality on the spart for the correlation coefficient: bivariate edgeworth series distribution, Journal of Statistical Computation and Simulation, 23:1-2, 41-51, DOI: 10.1080/00949658508810857

- Johnson, Kotz, and Balakrishnan, (1994), Continuous Univariate Distributions, Volumes I and II, 2nd. Ed., John Wiley and Sons.