< List of probability distributions < de Moivre distribution

The term “de Moivre distribution” has three meanings:

- In statistics, it’s another name for the normal distribution.

- In actuarial science, it’s used as a synonym for the uniform distribution.

- More generally, it is sometimes used to describe de Moivre’s theorem.

1. de Moivre distribution in statistics

In probability and statistics, the de Moivre distribution is another name for the normal distribution [1], which itself also goes by many different names [2] including “the law of error”, the “frequency law”, the “Gaussian curve”, and “Laplace-Gauss”.

The use of “de Moivre distribution” to describe the normal distribution is thought to originate with Freudenthal [3], who advocated the name because De Moivre was the first to define the distribution, in 1733 [4]. Although de Moivre’s contribution was not widely recognized at the time, Pierre-Simon Marquis de Laplace generalized de Moivre’s findings and included in his influential Theorie Analytique des Probabilites published in 1812 [5].

2. De Moivre Distribution in Actuarial Science

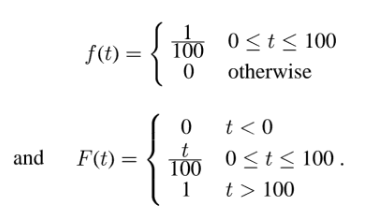

In actuarial science, a de Moivre is another name for the uniform distribution. For example, the de Moivre distribution is often used in relation to the actuarial study of uniform (de Moivre) distribution of deaths [6, 7].

For example [8], let T represent the time from birth until death of a random member of the population and assume that T follows a de Moivre distribution. Then:

The function F(t) allows us to calculate the probability a person will die by age t.

3. De Moivre’s theorem

French-born English mathematician Abraham de Moivre, a close confidant of Isaac Newton, made history by developing analytical trigonometry that is now universally known as “de Moivre’s Theorem”. He also explored concepts such as probability theory and the normal distribution. De Moivre credited his discoveries to Newton who was reportedly familiar with this theorem since 1676.

De Moivre’s Theorem ties together the topics of complex numbers and trigonometry. It states that for any real number x and any integer n:

(cos x + i sin x)n = cos(nx) + i sin(nx)

It can also uncover expressions for the nth roots of unity – or those special set of complex numbers z whose power yields 1:

z such that zn = 1

By expanding its left hand side equation and comparing parts, this theorem offers insight on both Euler’s identity

eix = cos x + i sin x

and the exponential law

(eix)n = einx.

De Moivre’s theorem can be derived from both of these equations although it preceded both formulae.

References

- Johnson, Kotz, and Balakrishnan, (1994), Continuous Univariate Distributions, Volumes I and II, 2nd. Ed., John Wiley and Sons.

- Stigler, S. M. (1999). Statistics on the table. The history of statistical concepts and methods. Cambridge, MA: Harvard University Press.

- Freudenthal, H. (1966b). Waarschijnlijkheid en Statistiek [Probability and Statistics]. Haarlem: De Erven F. Bohn.

- Daw, R. & Pearson, E. Studies in the History of Probability and Statistics. XXX. Abraham De Moivre’s 1733 Derivation of the Normal Curve: A Bibliographical Note. Biometrika Vol. 59, No. 3 (Dec., 1972), pp. 677-680 (4 pages)

- BIOSTATISTICS TOPIC 5: SAMPLING DISTRIBUTION II THE NORMAL DISTRIBUTION. Online: http://vietsciences.free.fr/khaocuu/nguyenvantuan/Topic05[1].Normal%20distribution.pdf

- Humphreys, N. ACTS 4301 formula summary. Lesson 1: Probability Review. Online: ttps://personal.utdallas.edu/~natalia.humphreys/MLC%20SP18/FORMULAE_MLC.pdf

- Randles, R. (n.d.). Chapter 4 – Insurance Benefits Section 4.4 – Valuation of Life Insurance Benefits. Online: http://users.stat.ufl.edu/~rrandles/sta4930/4930lectures/chapter4/chapter4R.pdf

- Hassett, M. & Stewart, J. (2006). Probability for Risk Management. ACTEX Publications.